What is the fixed rate mortgage cliff, and what can borrowers do to prepare?

If you’re among the borrowers who locked in a fixed-rate loan when rates were at record lows, then you’re in a more fortunate position than most other home owners with a mortgage.

Those who opted for a variable rate loan have seen their repayments climb over the past year, with the Reserve Bank hiking the cash rate target at every board meeting since May, pushing up repayments.

The average Australian borrower with a $600,000 variable rate loan now pays about $1155 more each month than they did in April last year before rates started rising, according to calculations using the Domain Home Loans repayment calculator.

RBA governor Philip Lowe has acknowledged that rate hikes have caused a “painful squeeze” on household budgets, but the full extent of that pain hasn’t hit fixed-rate borrowers just yet.

That’s because they’ve been insulated from the RBA’s steepest rate rise cycle in decades, some having locked in rates below 2 per cent while many variable-rate borrowers are now facing the prospect of rates above 6 per cent.

“They should be drinking champagne and rejoicing at the fact that they did lock in such low interest rates and everyone on a variable rate has been slugged already,” says Market Economics managing director Stephen Koukoulas.

But that’s all about to come to an end this year, with hundreds of thousands of home owners approaching what’s been described as the “fixed–ratecliff”.

The thought of falling off a financial cliff – or more accurately, climbing up one – sure sounds scary, but is it really as disastrous as it’s been made out, and is there anything fixed-rate borrowers can do to prepare?

What is the fixed rate mortgage cliff, and will I be affected?

Home owners who had the foresight to fix their loans when rates were cheapest will soon be in the same boat as everyone else, with the fixed-rate period on about 880,000 loans set to end this year.

When the fixed-rate period on a home loan expires, the interest rate typically reverts to the lender’s standard variable rate.

For borrowers who fixed in the past few years, those variable rates will be several percentage points higher thanks to the RBA’s incessant hikes over the past 10 months.

This phenomenon has been called a cliff because borrowers will face a sudden jump in repayments as they roll onto much higher variable rates.

How much will repayments increase when fixed-rate periods end?

The RBA has signalled it will increase the official interest rate at least two more times in the coming months.

Meanwhile, NAB, ANZ and Westpac expect the cash rate to peak at 4.1 per cent by May.

If the scenario forecast by those banks eventuates, fixed-rate borrowers could see their sub-2 per cent interest rates increase by up to 4 percentage points, based on the predicted amount the cash rate target could increase this tightening cycle.

In May 2021, the average borrower who fixed for three years or less was lucky enough to secure a rate of 1.95 per cent, according to the ABS.

If that borrower had the Australian average loan size of about $600,000, and their loan rolled onto a variable rate 4 percentage points higher – or 5.95 per cent – their monthly repayments would jump by $1375.

A borrower in that same situation with a $1 million mortgage – a more likely scenario for a recent home buyer in an expensive capital like Sydney or Melbourne – could see their monthly repayments increase by $2292.

How much your monthly home loan repayments could rise when your fixed-rate period ends |

|||

| Home loan amount | Monthly repayments – 1.95%* | Monthly repayments – 5.95%** | Increase to monthly repayments |

| $250,000 | $918 | $1,491 | $573 |

| $500,000 | $1,836 | $2,982 | $1,146 |

| $600,000^ | $2,203 | $3,578 | $1,375 |

| $1,000,000 | $3,671 | $5,963 | $2,292 |

| $2,000,000 | $7,342 | $11,927 | $4,585 |

|

Source: Domain Home Loans Repayment Calculator. The above table shows approximate amounts monthly home loan repayments could be when the fixed rate period on a home loan ends and a borrower rolls onto a variable rate. Estimates are based on a 30-year principal and interest loan, fixed for two years at 1.95 per cent in May 2021. Fees and charges are excluded, and this information is intended as a guide only. |

|||

Are people prepared for a sudden rise in home loan repayments?

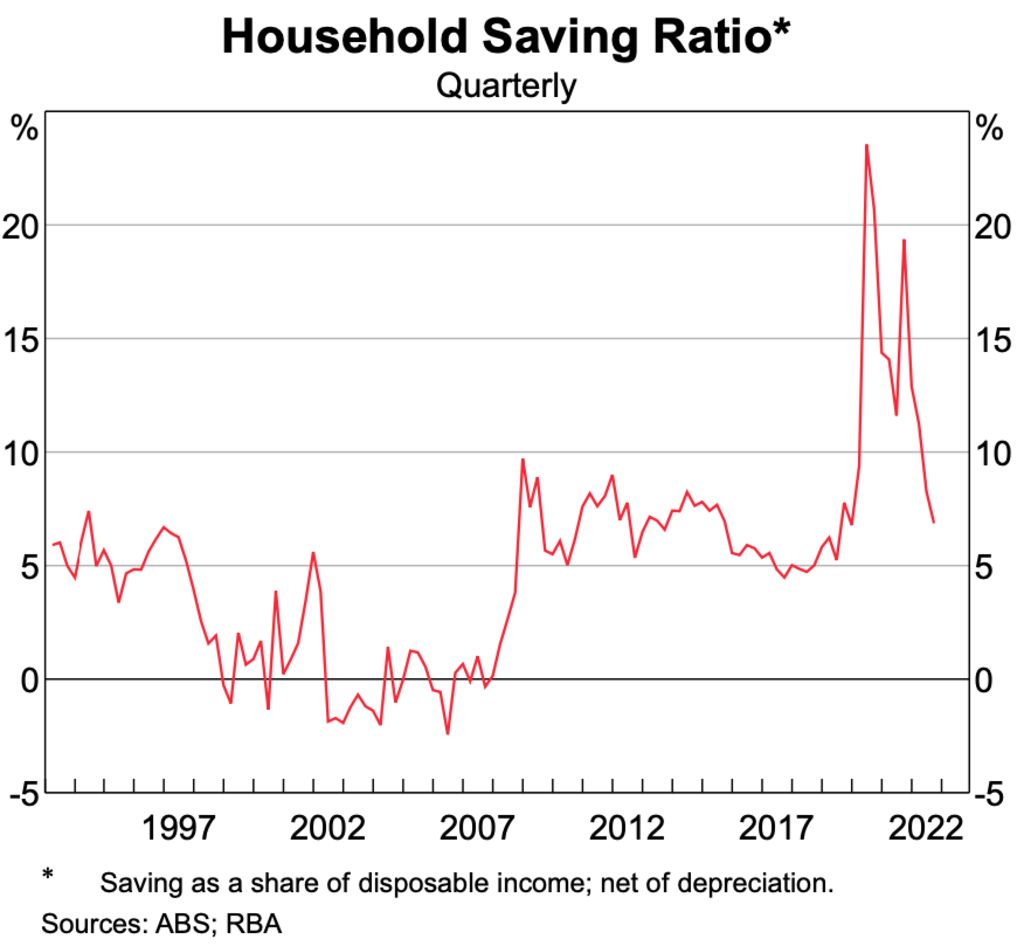

While this jump in repayments could come as a nasty shock to some fixed-rate borrowers, households have had almost a year to get ready, and ABS figures show incomes grew at the highest rate in a decade last year.

“The optimistic interpretation is fixed-rate borrowers have had plenty of time to prepare,” says AMP capital chief economist Shane Oliver. “Some of these people may have got their act together and squirrelled away money along the way that they can use to pay down their debt or pay the higher rate.”

But the tricky thing is, the cost of living has also soared during that time, with inflation rising 7.8 per cent in 2022 – well above the RBA’s target band of 2 to 3 per cent.

Meanwhile, savings levels have fallen with Australians spending a higher proportion of their incomes than in the past few years.

“There’s a degree of ‘revenge spending’ facilitated by savings that were built up during the pandemic,” says Oliver.

“But there’s another group of households that don’t have much excess savings at all.”

The RBA says some borrowers will need to start raiding their savings accounts to afford higher repayments.

“Some borrowers may need to reduce non-essential spending, save less overall and/or draw down on accumulated savings to service their mortgages,” the RBA said in its February Statement on Monetary Policy.

“Some households with low savings buffers and high debt relative to incomes will have to adjust their spending sharply.”

This adjustment to spending will put a dent in the economy, according to Koukoulas, but that’s not necessarily a bad thing.

“It’ll slow the economy down, there’s no question,” he says. “If people have to find an extra $1000 for their mortgage repayments, that’s $1000 that won’t be available to be spent elsewhere in the economy.”

However, less spending could ease demand on goods and services, helping to slow down inflation, which is essentially the whole point of raising interest rates. “That’s what the RBA is wanting to see,” Koukoulas says.

I’m on a fixed rate that’s ending soon, what should I do?

While no one wants to see their repayments go up, the best thing that fixed-rate borrowers can do is take action now.

“If you don’t know where to start, speak to a broker or call your bank and they will be able to tell you what your new rate will be in the current market and your new repayment,” says Domain Home Loans chief executive Kareene Koh. “There is no obligation to do anything yet but use these different free resources to get your facts straight.”

Rather than simply letting their fixed loan roll onto a variable rate and sticking with the current lender, Koh says borrowers should start investigating other options three months before their fixed rate period ends. For borrowers with fixed loans expiring mid-year, that means now.

“Do some ground work 90 days in advance and shop around. You may end up staying with your current bank but having a comparison loan up your sleeve helps your negotiation power.”

Rising interest rates have prompted more borrowers than ever to look for a better home loan deal, and with refinancing levels at record highs, according to the RBA, lenders are competing strongly to entice new borrowers.

“It is really competitive but like all things make sure you check the fine print,” says Koh. “There are lots of offers around like cashbacks and honeymoon rates to get customers to switch. Just make sure you balance this with other features that may be important to you like an offset account or redraw.”

Borrowers who stick with their existing lender hoping their loyalty will be rewarded may be disappointed, says Koh.

“Whilst the banks have got better at rewarding loyalty over the years, you should never assume this is the case,” she says. “Most customers should be active managers of their home loan if they want a better deal.”

How can I can save money to prepare for higher repayments?

Beyond refinancing, there’s plenty that borrowers can do to put themselves in the best position to meet their higher repayments.

“Finances are just like fitness, the earlier you get started, the easier it gets,” says Koh. “Rather than waiting for a change to happen, take the time now to build your fitness and be ready for your change in repayments when it happens. That way you have done the hard work of trimming where you need to, working out any pain points or making any major life adjustments if that is required.”

Review your household budget – Depending on your situation, this could mean eliminating unnecessary spending, putting off big purchases like a new phone or car, cancelling subscriptions you don’t use or shopping around for a cheaper energy or insurance provider.

Make lifestyle adjustments – Cutting back on “luxuries” like dining out, alcohol or takeaway food and coffee could make a difference. Even switching to generic brands or looking for half price items at the supermarket could reduce your grocery bill.

Use an offset account – One benefit of coming off a fixed-rate loan is that variable mortgages often come with an offset account, whereas fixed-rate loans typically don’t. Money stashed in an offset account won’t earn borrowers interest like a typical savings account, but instead will be deducted from the home loan balance when calculating the interest borrowers need to pay, reducing monthly repayments. In other words, the more money you save, the less interest you’ll pay.

Ask for help – If you’re having trouble meeting your repayments, contact your lender. Banks have hardship teams whose job it is to help you keep a roof over your head if you run into financial difficulty. It may be possible to defer repayments, set up a payment plan, switch to interest-only payments or even extend your loan term to reduce your repayments. Lenders don’t want to force you to sell your home, and this generally only happens as an absolute last resort.

Remember that small changes can have a big impact over time, especially when multiple strategies – like refinancing, budgeting and saving – are combined. And although everyone’s situation is different, the most important thing is that fixed-rate borrowers start taking action rather than sitting back and doing nothing.

“Don’t bury your head in the sand,” Koukoulas says. “Confront the issue head on.”

We recommend

States

Capital Cities

Capital Cities - Rentals

Popular Areas

Allhomes

More