Housing affordability: Rise of Bank of Mum and Dad fuels inequality in hot market

We knew house prices were booming, but it’s a shock to see how much.

Anyone trying to get into the market in Sydney this year has watched the price of a median house soar by $103,000 in only three months. In Melbourne, the jump was nearly $45,000.

Record prices are a reminder we still have a housing affordability crisis, even if it has slipped from public debate in recent years.

And the boom risks pushing home ownership even further out of reach for many, making inequality worse.

UNSW housing researcher Chris Martin is blunt about the problem: although ultra-low interest rates make it cheap to pay off a mortgage, that’s no help to someone who hasn’t got a deposit.

With the median Sydney house price now above $1.3 million, on the latest Domain House Price Report figures, a 20 per cent deposit would be north of $260,000.

Melbourne’s median house price is now almost $975,000, for which a deposit would be nearly $195,000, after low interest rates and pent-up post-lockdown demand pushed prices up.

That’s only the median house – forget living in a popular inner-city neighbourhood on that budget.

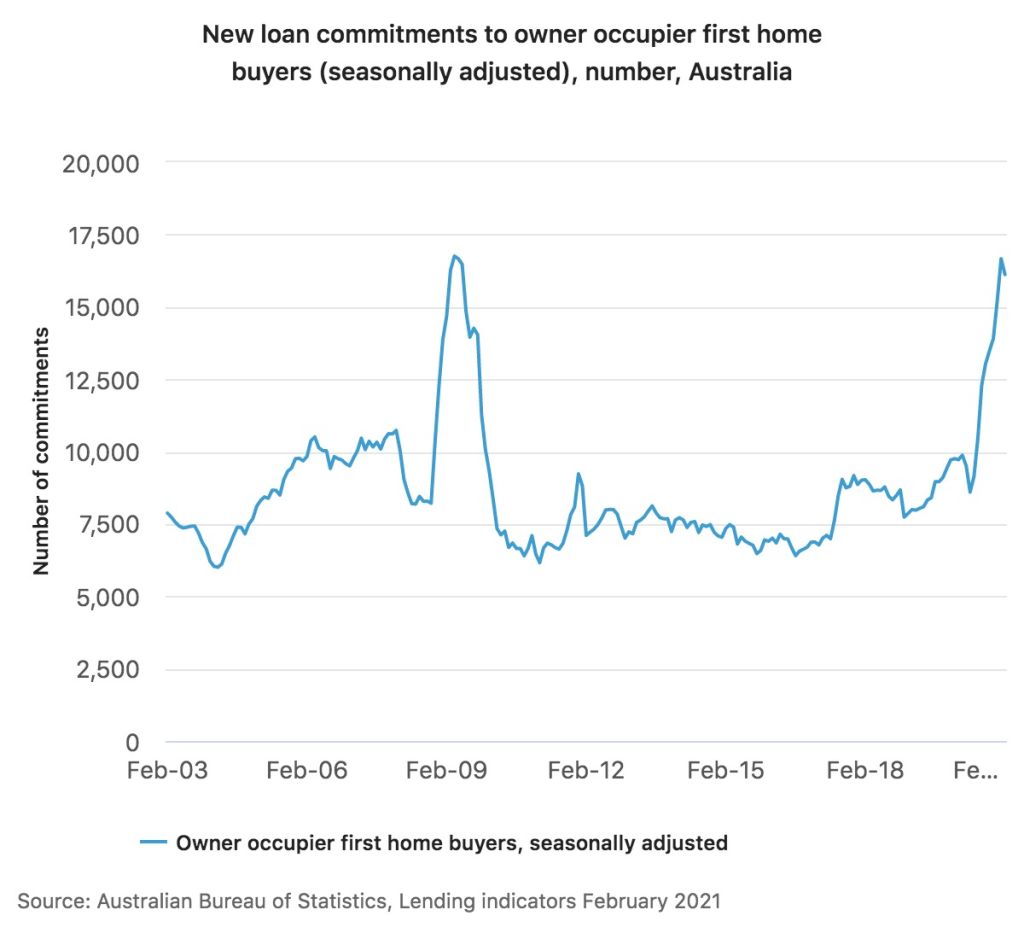

The average full-time Australian employee is paid about $92,000 a year, so even for a couple, how can first-home hopefuls save that kind of deposit? How much further will house prices have run away by the time they do? And how did the number of first-home buyers reach the highest level in a decade last year?

“Over the last few months, there have been first-home buyers getting back in [to the market] in a pretty big way,” said Dr Martin, a senior research fellow at the UNSW City Futures Research Centre.

“But doing that on the back of rising house prices makes me think they are doing it with a lot of help from people who are already in.”

That is, the Bank of Mum and Dad, who may have bought their own houses during an era of low unemployment, rising wages, government policies to build public housing units and sell them to residents, and rental laws that discouraged investment property ownership, he said. Even if interest rates were higher, they could get onto the ladder in the first place.

There are no official figures quantifying the help parents or grandparents provide in the form of guarantees or cash gifts, but mortgage brokers have reported families helping adult kids even in lower-priced suburbs.

Dr Martin notes that someone saving a deposit on their first home is taxed on their income, but someone who owns a home that increases in value is not taxed on their gains when using that equity to offer a guarantee for a family member.

“It’s a further concentration of housing wealth and housing access and it means a more unequal housing market,” he said.

“It means a more unequal society.”

The last time housing affordability was on the agenda as a five-year bull run peaked in 2017, the issue was largely limited to Sydney and Melbourne, with NSW Premier Gladys Berejiklian declaring it the “biggest issue people have across the state”.

Now, affordability is a broader problem, with house prices soaring around the country – up more than 9 per cent in three months in Canberra and Darwin, and 7.6 per cent in Hobart – and city-slickers taking their high wages to regional Australia to work remotely, and competing with locals for limited housing supply.

Governments have stepped in with politically popular programs to help first-home buyers, mindful of the swathe of the voting population who now rent.

The federal First Home Loan Deposit Scheme has had strong take-up, allowing purchases of modest homes with only a 5 per cent deposit without paying lenders’ mortgage insurance and offering a similar benefit to a parental guarantee for buyers without family help.

It’s capped at 10,000 places a year for established homes, and another 10,000 for new builds, compared to the roughly 100,000 first-home buyers who purchased annually when the scheme was introduced.

State governments have offered various stamp duty discounts for entry-level homes and cash grants for new builds, while the federal government also introduced a pandemic-era HomeBuilder program of grants for new construction.

Demand-side stimulus is welcome to those who were close to being able to buy, or could bring forward plans to buy, but research has shown grants push up prices by the value of the grant while doing little to help lower-income households.

And the temporary stimulus boost coincided with a fall in investor purchases during the COVID-era rental eviction moratoriums.

Despite the popularity of stimulus programs, ANZ senior economist Felicity Emmett said, grants for new builds would be largely used on the outskirts of major cities such as Sydney or in regional areas.

She forecast capital city housing prices to soar 17 per cent this year, a rise she said could lock some aspiring first-home buyers out as they struggled to save a deposit.

“For a first-home buyer who doesn’t have access to the Bank of Mum and Dad, it’s really virtually impossible to buy in a capital city,” she said.

“It’s only a matter of time before we see those cohorts like first-home buyers drop away a little bit. They’ve obviously benefited over the last year from some of the specific support packages.

“Many of those first-home buyers are more and more accessing the Bank of Mum and Dad, which is concentrating the wealth impact and really highlighting how things like COVID can increase inequality.”

Charter Keck Cramer director Angie Zigomanis noted the deposit gap was a moving target, with some banks more willing than others to lend to buyers with small deposits.

“As prices increase it becomes harder and harder to meet that deposit because the lower interest rate lets you leverage up but you still have to pay the deposit up-front,” he said.

“It depends on bank policy and whether the bank will let you borrow on a smaller deposit and a higher loan-to-valuation ratio.”

Already home loans to first-time buyers are starting to edge down, although it’s too soon to tell if this is more than a temporary blip.

A key measure of sentiment is also ticking down, with fewer survey respondents saying now is a good time to buy a dwelling, according to the latest Westpac-Melbourne Institute Index of Consumer Sentiment.

But forecasters expect prices to keep rising this year, even if not at the same ferocious pace.

Price rises mean first-home buyers will face decisions about compromising, Domain senior research analyst Nicola Powell said.

“Affordability is so challenged and affordability is biting for first-home buyers,” Dr Powell said. “It gets to the point where buyers have to make a compromise.”

She notes the rise of the “rentvestor”, where city dwellers rent where they want to live and buy an investment property in a regional town in the hopes it will increase in value enough to sell later and put the profit towards a city deposit.

She added that apartment price growth had been less extreme than that of houses. Unit prices are up 2.2 per cent in each of Sydney and Melbourne over the last quarter, to respective medians of $751,000 and $569,000.

Of course, the mums and dads now helping their adult offspring had to make their own compromises and save up for a home.

And anyone trying to save money will benefit from not spending money – a smattering of Melburnians managed to break into the market late last year after being banned from going out to restaurants or even having a haircut during the city’s extended lockdown.

But there are important differences now.

Reserve Bank research in 2017 found the options a first-time buyer could consider were further from the city than two decades previously, a trend most pronounced in Sydney, and had fewer bedrooms than in the past, an issue across all capital cities.

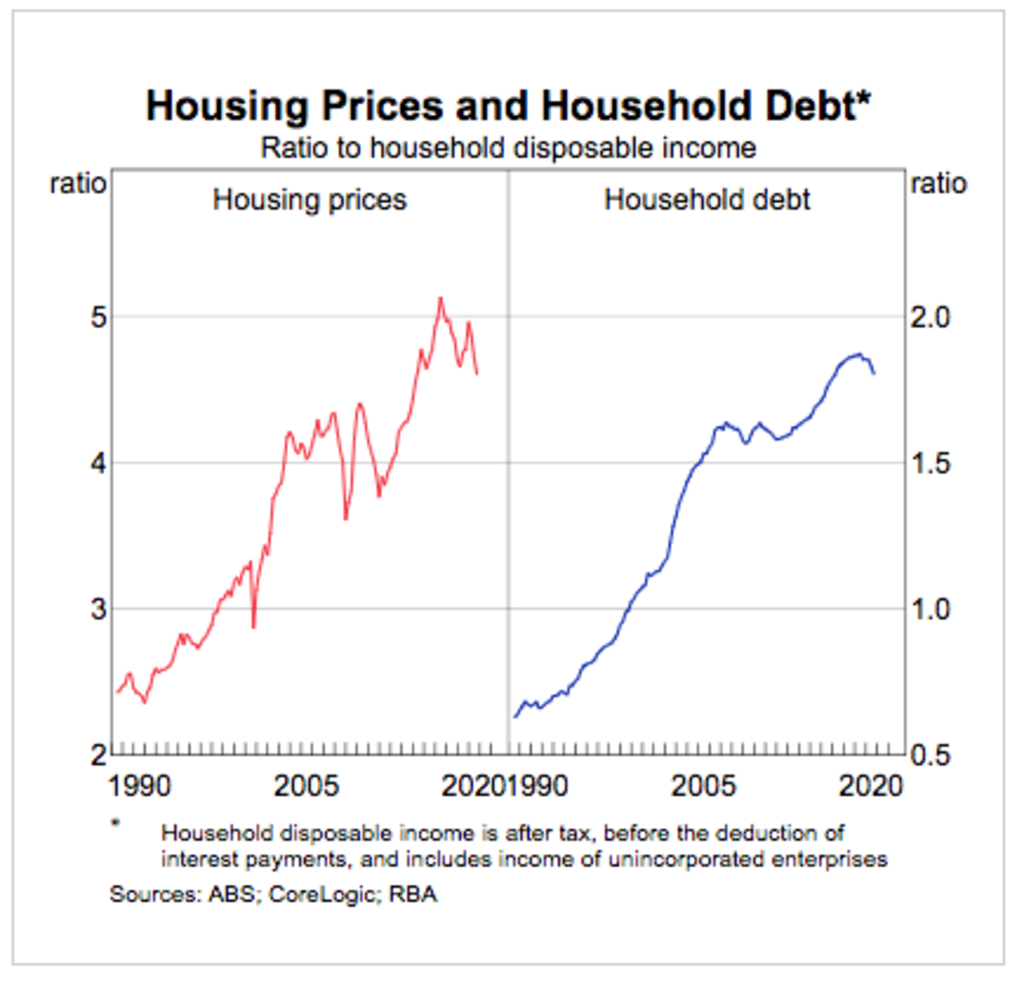

As interest rates have fallen, housing prices have risen relative to incomes. House prices were little more than double disposable incomes in 1990, but are now closer to five times on average – and more in major capitals.

Rates of home ownership have fallen over time, with frustrated young renters pointing to the classic avocado toast example. Yes, not spending $22 on a cafe brunch will help you save, but what use is it when a Sydney house deposit costs 11,901 cafe brunches?

And if the bank regulator steps in to make it harder to get a home loan, as in 2017 when it curbed lending to investors, it could make it harder for the owner-occupiers fuelling the boom to buy in.

Even the industry recognises the scale of the challenge, working at the coalface of efforts to plan the right supply to meet the needs of Australian households.

Inner-city apartments might have emptied as international students were locked out when borders closed at the start of the pandemic, but they can be a poor fit for families with children.

“We recognise that affordability is a serious issue right across Australia, particularly in our capital cities where supply continues to be an issue, even while our immigration is at record low levels,” Mirvac chief executive Susan Lloyd-Hurwitz said.

Stockland communities chief executive Andrew Whitson echoed this sentiment, saying: “Despite migration at the lowest levels in decades, housing affordability has remained a challenge for the industry and government at all levels. Governments across Australia have a once-in-a-generation opportunity to catch up on decades of underbuilding.”

University of Melbourne housing research fellow Kate Raynor emphasised the need to invest more in social housing as the ranks of renters swell.

She said she would also like to see more support for build-to-rent homes, where institutional owners instead of mum-and-dad landlords own whole apartment towers, but only if they have a regulated affordable housing component.

She called demand-side grants “counterproductive”.

“They have a perverse outcome for housing affordability,” Dr Raynor said. “We are throwing money at making the problem worse.”

We recommend

We thought you might like

States

Capital Cities

Capital Cities - Rentals

Popular Areas

Allhomes

More