Saving for a home deposit? Here’s how much more you’ll need, despite the downturn

Australians saving a house deposit need to have tens of thousands of dollars more than they did just three years ago, even as prices fall in the market downturn.

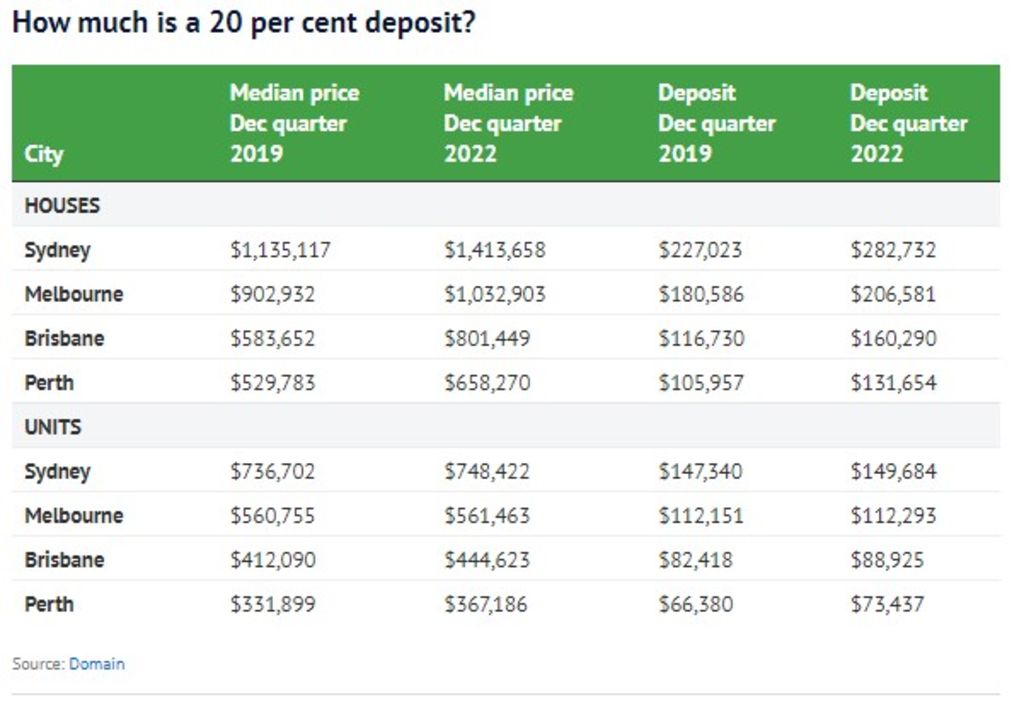

The savings required for a 20 per cent deposit ballooned during the pandemic property boom, which saw house prices skyrocket in Sydney and Melbourne, and are still up on 2019 levels.

It has left a growing number of buyers asking for help from “the bank of mum and dad”, experts say. Others are willing to pay lenders’ mortgage insurance, required for deposits of less than 20 per cent – which now sit at more than $200,000 for the median priced house across Australia’s combined capital cities.

Sydney house prices have declined 11.3 per cent from their market peak early last year, but buyers still need to save about $55,700 more than they did in the December quarter of 2019 – while facing rising mortgage rates.

House prices in Sydney skyrocketed from a median of about $1.14 million in the December quarter of 2019, to more than $1.4 million three years later, increasing the size of a 20 per cent deposit from $227,023 to $282,732. On the other hand, the NSW government now allows first home buyers to opt out of upfront stamp duty for a smaller annual land tax payment.

In Melbourne, house prices have dropped 5.6 per cent since their late 2021 peak, but a 20 per cent deposit is almost $26,000 more expensive than pre-COVID times.

Melbourne’s median went from just over $900,000 in late 2019 to more than $1.03 million late last year, meaning a 20 per cent deposit went from $180,586 to $206,581.

Potential unit buyers may have better luck, only needing an extra $2344 in Sydney and barely any more in Melbourne.

Grattan Institute economic program policy director Brendan Coates said saving a 20 per cent deposit was still one of the biggest hurdles for home buyers, even as prices fell.

“Saving for a deposit is a way bigger problem than it has been historically,” Coates said. “Without family support it becomes much harder to get into the market.”

Coates said people without family help were less likely to be able to stretch themselves financially to get into the market, or to buy a bigger or nicer home, creating a larger divide between the “housing haves and have-nots”.

“Having a wealthy family becomes a type of insurance because [buyers know they] can get help if things go south, and they can’t afford repayments,” he said.

Sydney-based Equilibria Finance managing director and mortgage broker Anthony Landahl said some buyers were surprised by the size of deposit now required.

“Some people come to us not realising the size of the deposit they’ll need, so we need to educate them and set them up with a savings plan, so they can save for 12 months and come back,” Landahl said.

Many buyers were receiving financial gifts from family, or using a family guarantee which would enable them to borrow more, he said. Others were using government schemes, or paying lenders mortgage insurance, so they could purchase with a smaller deposit.

James Algar, of Mortgage Choice Dee Why, said many parents had been offering financial support, so their children could purchase nearby.

“The bank of mum and dad seems to have featured significantly more over the past couple of years,” Algar said. “Parents were saying ‘we’re happy to give you some money to help out and keep you close’.”

Buyers were seeing the downturn as opportunity to get into the market for less, but were still having to ask their parents for help, he said.

Melbourne-based Foster Ramsay Finance’s Chris Foster-Ramsay said fewer buyers were now saving a 20 per cent deposit, compared to pre-pandemic times.

“There’s probably an element of ‘that’s just too much’,” Foster-Ramsay said.

“A deposit of $50,000 or $100,000 is an okay amount … but when you’re pushing to save double that, buyers think there’s got to be an easier way to save by asking for help.”

More children were relying on their parents, or inheritance money, when buying a home, Foster-Ramsay said.

The federal government’s First Home Guarantee was also still very popular, as were the state government’s stamp duty exemptions and concessions.

We recommend

States

Capital Cities

Capital Cities - Rentals

Popular Areas

Allhomes

More

- © 2025, CoStar Group Inc.