Seven graphs that show why it's so hard to find cheap house prices right now

Despite warnings of the biggest recession since the 1930s, Australia’s house prices barely fell this year and are already rising on the back of rock-bottom interest rates and unprecedented stimulus.

While the lucky country managed to come through the crisis with the economy in better shape than initially feared, many home buyers have been surprised to find that a downturn doesn’t mean a discount.

But why are house prices seeming to defy gravity? Here are seven graphs that explain.

1. Interest rates dropped

Interest rates have been slashed to rock-bottom levels this year, as the Reserve Bank tries to support the economic recovery.

Although banks have not passed on the entire cut, homeowners can get fixed-rate deals as low as 1.99 per cent per annum.

“The drop in interest rates has been larger than people realise,” ANZ senior economist Felicity Emmett said. “People have switched from variable to fixed so they’re getting a very significant decline in interest rates.

“That means that people can borrow more.”

Home buyers then turn up to auction with a bigger budget, bidding up prices.

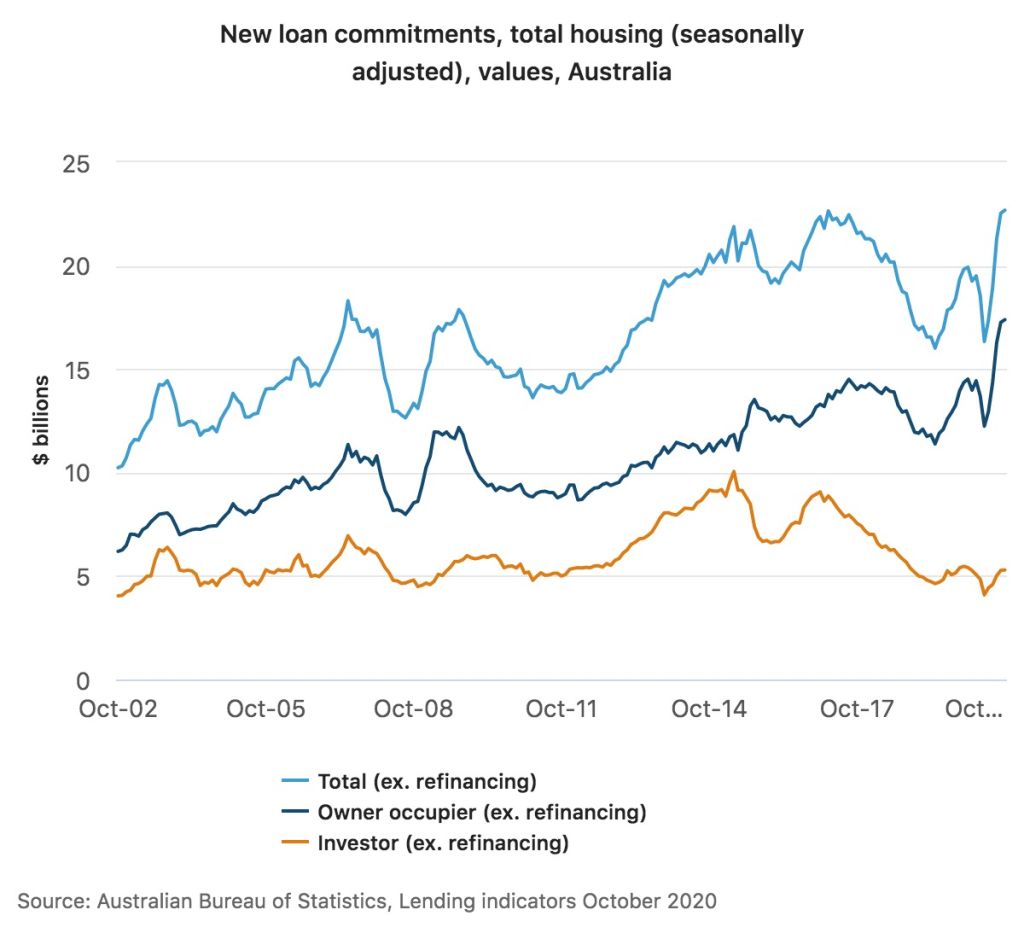

2. Home lending soared

The amount of money lent to buy homes or refinance has been rising, reaching a record high in October.

Although it can still be challenging to get a loan approved, with buyers needing to prove they have a steady income and good control over their expenses, banks are willing to lend – especially to low-risk borrowers.

Again, the Reserve Bank is helping. It has offered up to $200 billion in cheap money to commercial banks, to help them lend to small businesses and keep mortgage interest rates down.

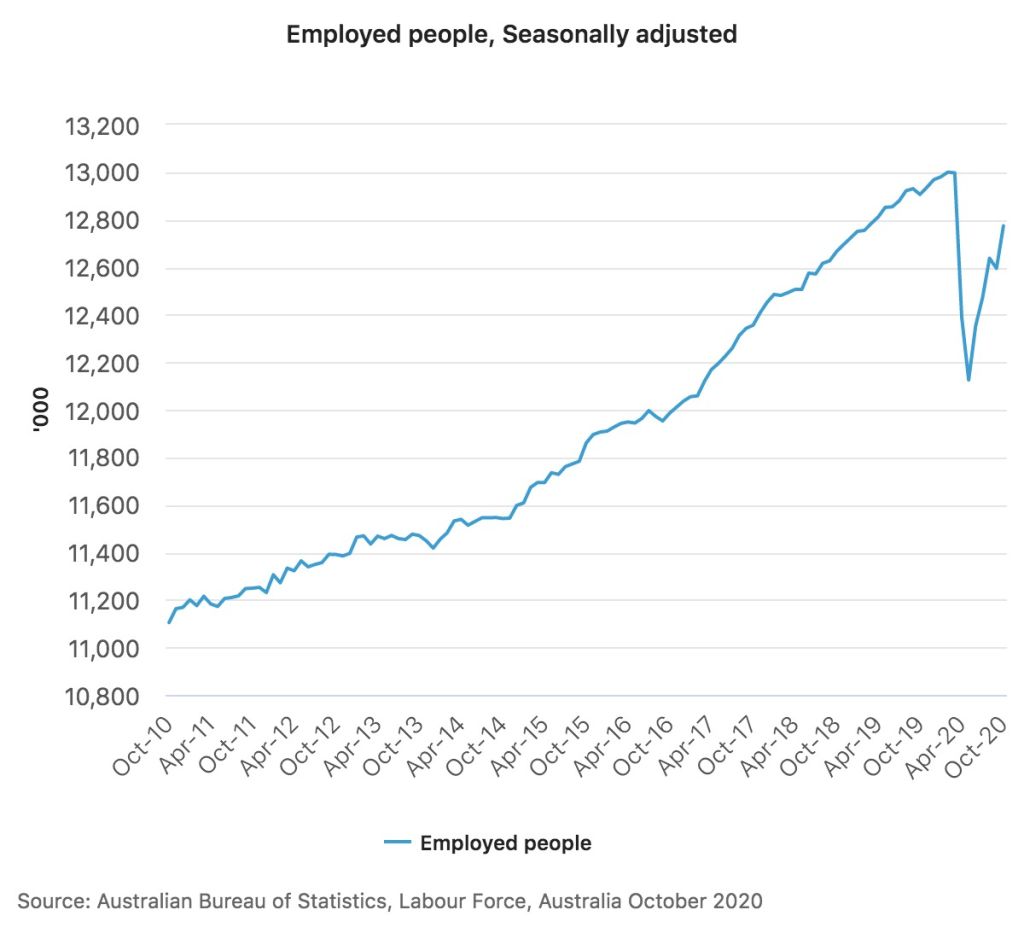

3. The job market improved

Despite a sharp jump in unemployment when state and federal governments put the economy into hibernation to slow the spread of COVID-19, workers are starting to return to their jobs as the economy re-opens.

“We did think that the labour market would be much harder hit than it has been, and it has also recovered much more quickly than we expected,” Ms Emmett said.

Plus, most of the job losses were in low paid industries such as hospitality, where workers are less likely to own a home or to be on the verge of buying one, she said.

“The labour market has been very unevenly affected, and people who are either home owners or aspirational home owners haven’t really been as badly affected as people who rent.”

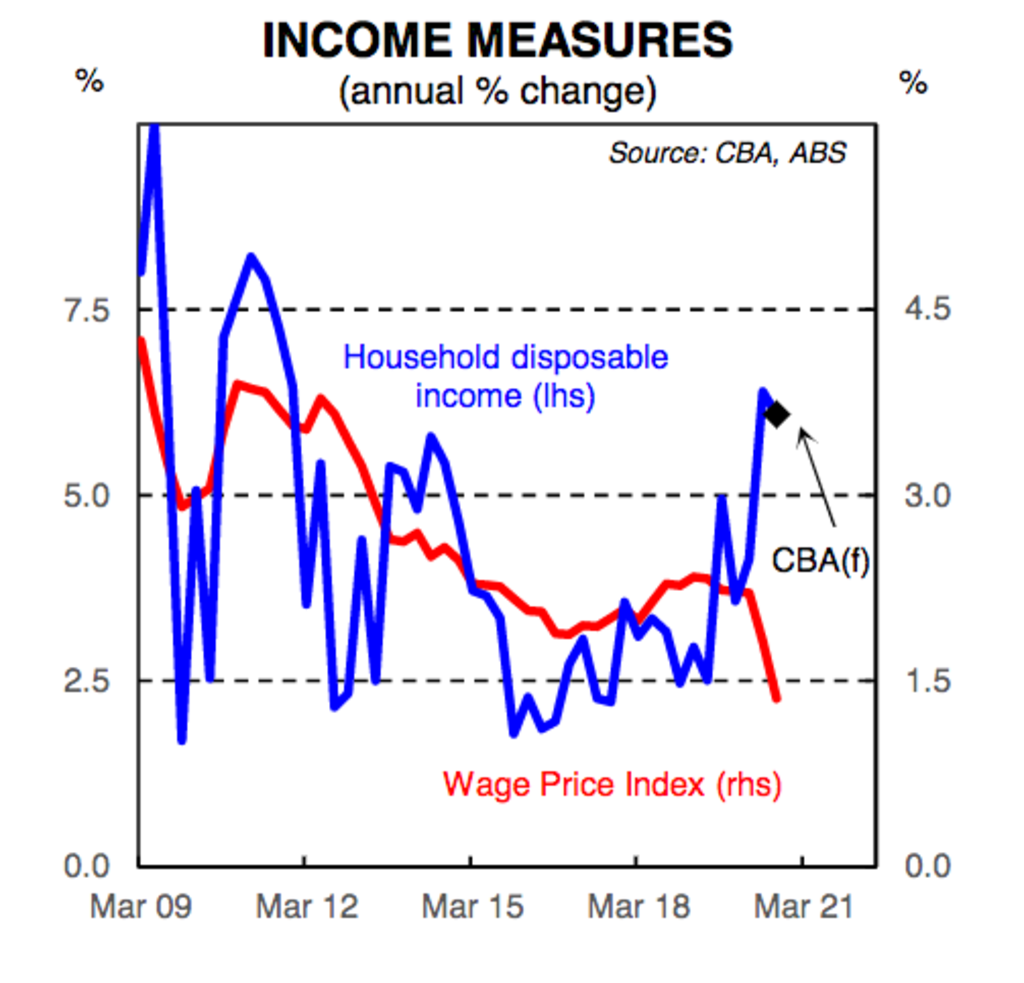

4. Disposable income rose

Although wages growth is low, some workers who have kept their jobs have rising disposable incomes.

Tax cuts in the recent federal budget are boosting take-home pay, with CBA estimating a full-time worker on an average salary will get a 1.6 per cent pay increase in fiscal 2021 without any change to their wage due to lower taxes.

Some households have saved money by not being able to travel overseas or dine out as much. Households have saved almost $119 billion over the past year, part of which could flow into property, pushing up prices.

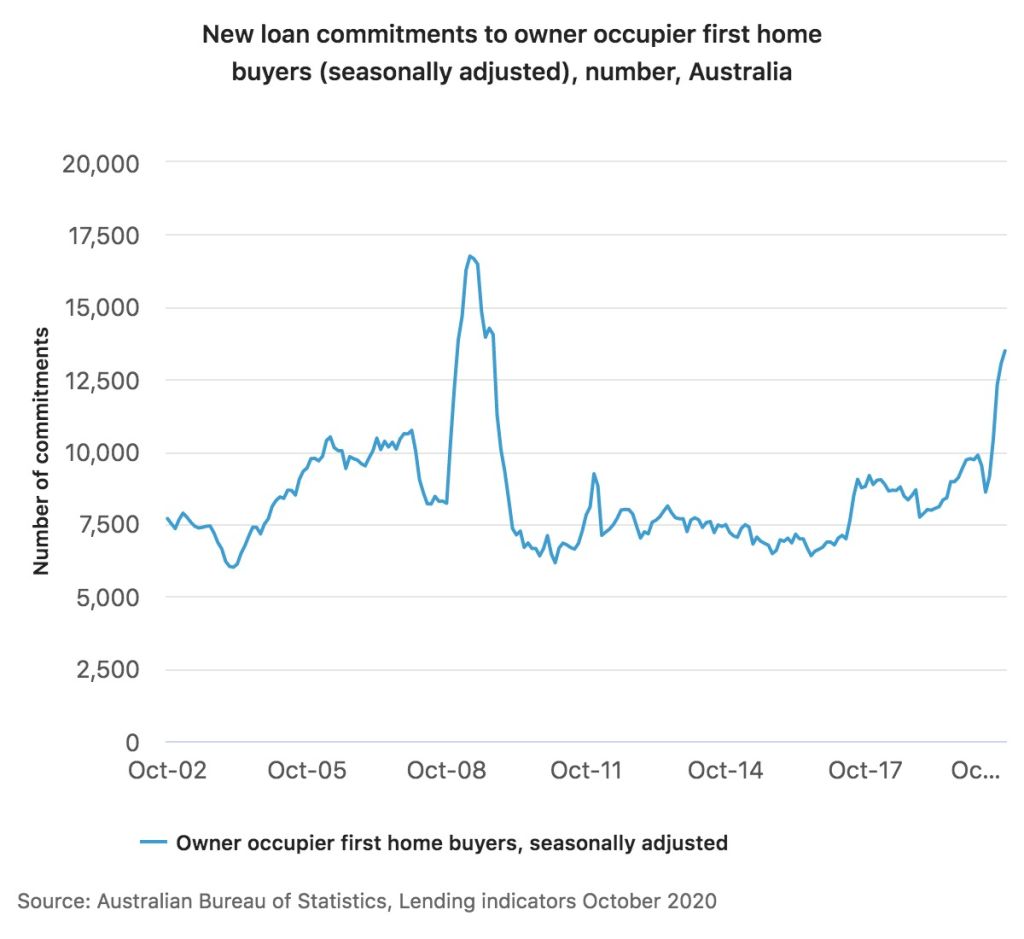

5. First-home buyers got a break

First-home buyers have been rushing into the market this year armed with grants and discounts in the biggest buying spree since a tripling of the first home owner grant in the GFC.

Stamp duty discounts for lower-priced properties were already on offer in some states, with Victoria recently announcing further tax discounts and NSW planning a move away from stamp duty to a land tax.

Buyers have been taking advantage of the federal government’s First Home Loan Deposit Scheme to buy with a deposit as low as 5 per cent while avoiding lender’s mortgage insurance.

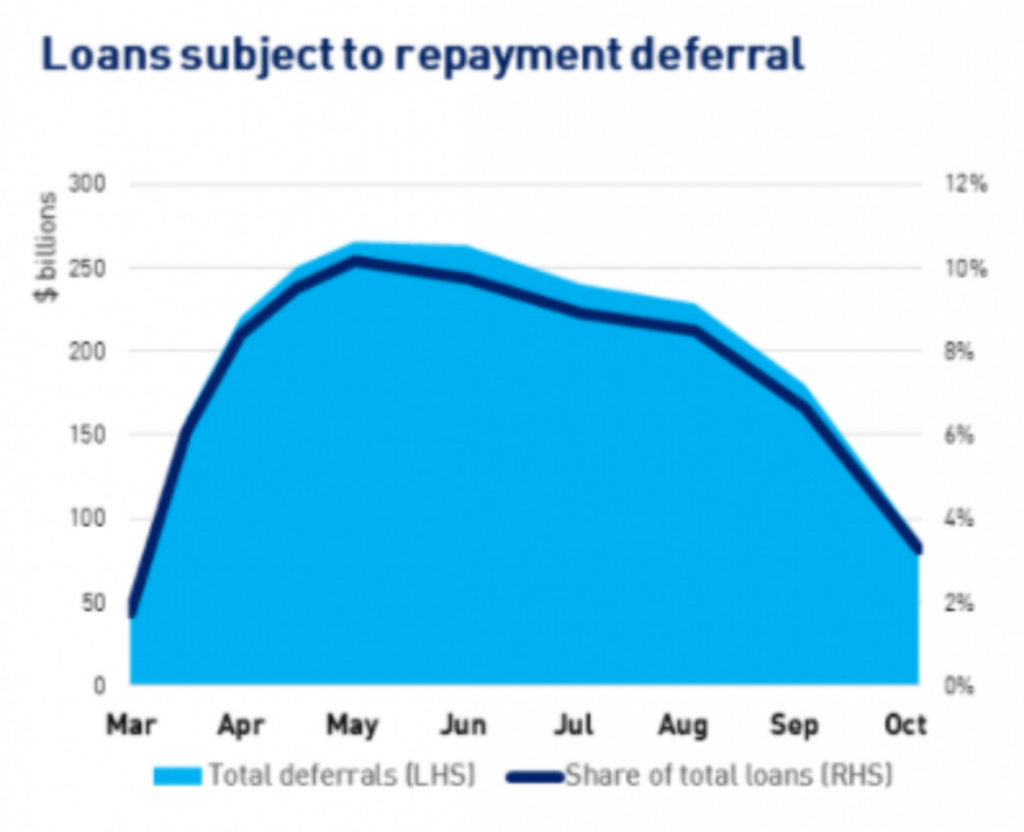

6. Mortgage holidays helped

Stimulus introduced at the height of the crisis has been working.

Borrowers who lost work in autumn were able to defer their mortgage payments, avoiding a wave of distressed selling that could have pushed property prices down.

The JobKeeper and JobSeeker payments also helped keep households afloat.

Sydney buyer’s agent Michelle May had inquiries early in the year from “opportunists” looking to pick up a bargain.

“They were telling me, I’m only buying if I get this kind of a return, or this kind of discount,” the principal of Michelle May Buyers Agents said.

But bargains were thin on the ground, she says, comparing it to the previous price downturn in 2017-18.

“Vendors who didn’t have to sell simply held on, and the same thing happened with covid, and that’s what is primarily driving this increase in prices,” she said.

Now, buyers have realised discounts are unlikely as they turn up at open homes with queues to get in, or attend auctions such as a recent inner west sale with 22 registered bidders, leading to a fear of missing out, she said.

“I’m seeing a lot of frustration and dread and FOMO.”

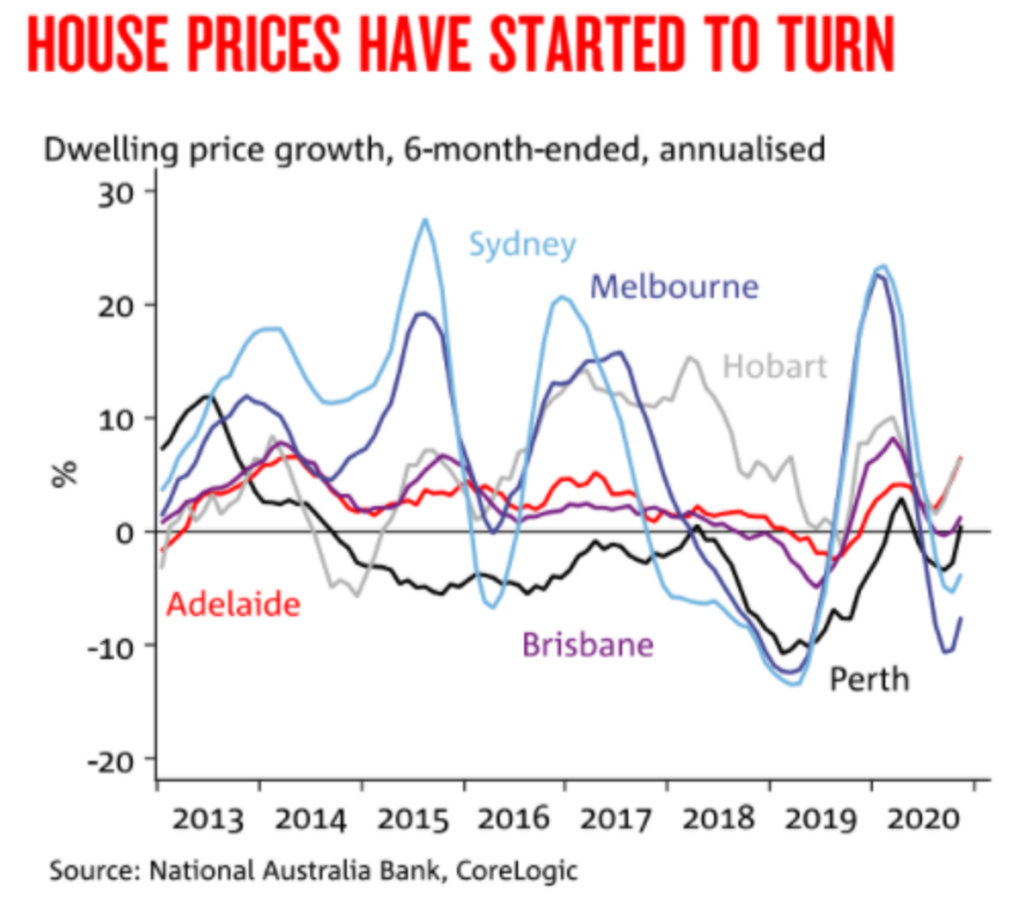

7. Prices have ticked up

Home values are now ticking up in every capital city, even Melbourne after its long lockdown, November data from CoreLogic shows.

It follows the September quarter Domain House Price Report that found house prices rose in every capital city except Melbourne, which was flat.

A string of economists have upgraded their forecasts and no longer expect to see price drops of 10 per cent to 15 per cent, instead tipping prices to lift.

Ms Emmett said there is a risk that the end to fiscal stimulus over the next few months could put pressure on the market, along with low population growth and elevated unemployment.

“There are a number of headwinds for the housing market,” she said.

“On the upside though, there does seem to be a lot of momentum. We’ve seen auction clearance rates are very solid, there’s certainly anecdotes of houses going well above reserve.

“This is creating very positive sentiment, and it’s possible that there is an element of FOMO re-entering the market.”

We recommend

States

Capital Cities

Capital Cities - Rentals

Popular Areas

Allhomes

More